TL;DR:

- Edmonton’s construction boom in 2026 is driven by strong public funding and sector-specific growth.

- Industrial and infrastructure projects are leading, while residential starts are moderating.

- Labor shortages are pushing adoption of advanced technologies like BIM and modular construction.

Edmonton is sitting on one of the most active construction pipelines in its history, with 167 active projects worth $43.3 billion underway right now. But the headline numbers only tell half the story. Beneath the record-breaking volume, project managers are navigating a market that rewards strategic thinking over simple participation. Labor constraints are tightening, certain sectors are cooling after a historic surge, and contractors are becoming increasingly selective about which projects they take on. If you are planning projects in Edmonton for 2026 and beyond, understanding the nuances behind the growth is just as important as tracking the growth itself. This guide covers sector-specific trends, technology shifts, and the practical intelligence you need to make better decisions.

Table of Contents

- The scale and nature of Edmonton’s 2026 construction boom

- Major drivers: Population, capital budgets, and policy shifts

- Sector deep-dive: Navigating obstacles and sector shifts

- Technology, labor, and procurement innovation

- What most Edmonton guides miss: The opportunity in selective growth

- Take your next step with the right construction partner

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Edmonton’s boom in context | 2026 features record-setting project numbers but notable shifts in sector performance and risks. |

| Funding and policy drive growth | Investment from city and province, plus streamlined municipal policies, underpin active projects and infrastructure upgrades. |

| Sector trends to watch | Industrial and ICI construction lead, while residential sees a post-boom slowdown in Edmonton’s diversified market. |

| Innovation combats labor crunch | Managers facing workforce and cost pressures are rapidly adopting AI, BIM, and advanced procurement methods. |

| Smart project selection wins | Success in 2026 depends on choosing the right sectors, partners, and technologies as much as capitalizing on high project volumes. |

The scale and nature of Edmonton’s 2026 construction boom

The numbers are genuinely hard to ignore. Record housing starts in 2025 rose 16% year over year, and the city’s overall construction pipeline is the largest it has ever been. But smart project managers know that understanding what is being built, not just how much, is where the real intelligence lives.

Here is a breakdown of Edmonton’s active construction segments in 2026:

| Sector | Activity Level | Key Driver |

|---|---|---|

| Institutional (schools, hospitals) | Very High | Provincial capital budget |

| Commercial | High | Population growth, retail demand |

| Industrial | Very High | Logistics, small-bay demand |

| Infrastructure (roads, LRT) | Very High | Municipal and provincial programs |

| Residential | Moderating | Post-surge inventory correction |

The industrial market deserves particular attention. Vacancy rates have dropped below 3%, and small-bay industrial space (units under 10,000 square feet used by trades, e-commerce, and light manufacturing) is being leased faster than it is being built. Positive absorption, meaning more space is being occupied than delivered, has been a consistent pattern across the Edmonton metro area for several quarters. This is a signal that demand is structural, not speculative.

Residential construction tells a different story. After the record run in 2025, housing starts are tapering. Speculative inventory built during the surge is now working through the market, and population growth, while still positive, has stabilized somewhat. For project managers whose pipeline includes residential work, this shift is worth building into your capacity planning and risk assessments.

Non-residential construction, on the other hand, shows no signs of slowing. The ICI sector (institutional, commercial, and industrial) and construction service types tied to public infrastructure remain strong. Our own recent Edmonton projects reflect this pattern directly, with road maintenance, concrete, and site prep work continuing at a high pace across the region.

Key highlights for your planning:

- Industrial vacancy below 3% is a reliable indicator of sustained build demand through at least mid-2027

- ICI projects represent the largest share of Edmonton’s $43.3B active pipeline by dollar value

- Residential starts are moderating, not collapsing, with multi-family continuing better than single-family

- Infrastructure funding is locked in, making public sector work more predictable than private

- Edmonton’s market shift points toward a more balanced mix of project types over the next 18 months

The practical takeaway here is that diversification across sectors is not just smart risk management. It is increasingly how the most resilient local contractors and project managers are structuring their 2026 pipelines.

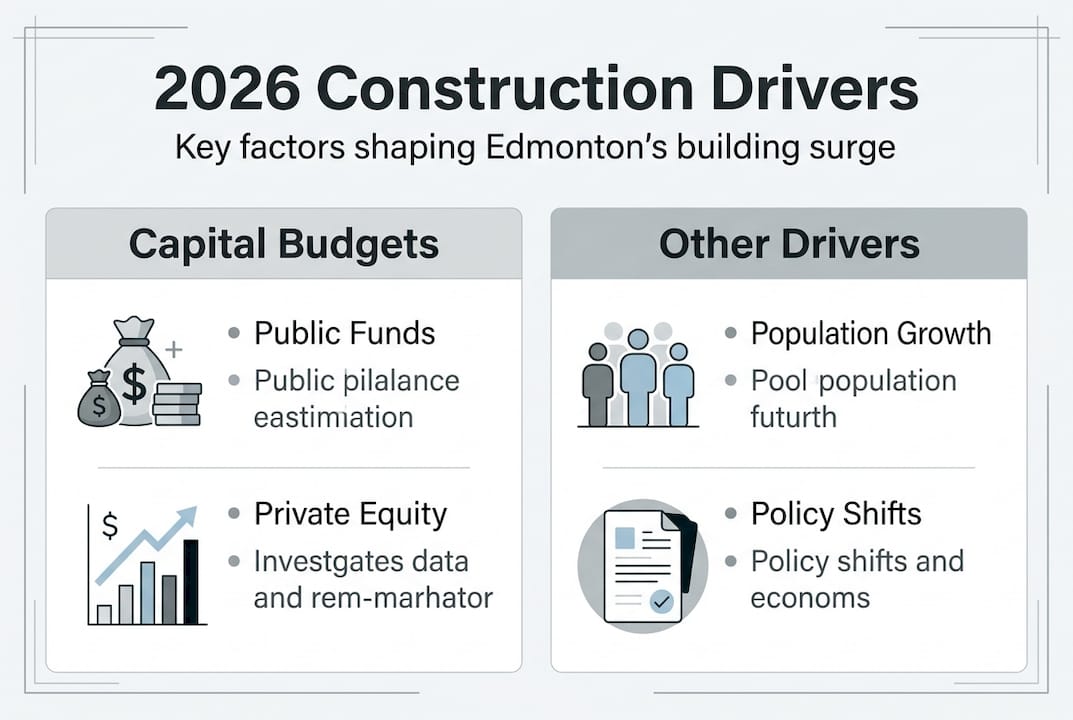

Major drivers: Population, capital budgets, and policy shifts

But what is powering this surge in projects? The answer lies in the funding landscape and key policy shifts.

The single largest structural driver is public capital investment. Alberta’s provincial capital plan commits $28.3B over three years, with 109 projects active in 2026 across the Edmonton region. The City of Edmonton adds its own annual infrastructure budget of $1.5B on top of that. When you combine both levels of government, you get a funding floor that keeps public sector project activity elevated regardless of private market conditions.

Where is the money actually going? Here is a simplified comparison:

| Funding Source | Annual Commitment | Priority Areas |

|---|---|---|

| Province of Alberta | Portion of $28.3B (3-yr) | Schools, hospitals, LRT, highways |

| City of Edmonton | $1.5B/year | Roads, utilities, parks, transit |

| Federal Programs | Variable | Affordable housing, green infrastructure |

Population growth has been a major amplifier. Edmonton absorbed significant interprovincial migration over the past two years, and while the pace is moderating, the cumulative demand it created for schools, healthcare facilities, and roads has already been baked into approved capital budgets. Those projects are now moving to execution, which is why you see so many institutional builds in the active pipeline.

On the policy side, the city has made deliberate moves to streamline zoning and permitting, particularly for infill and multi-family residential. This does not mean the process is fast, but it is measurably faster than three years ago. For managers working on urban residential or mixed-use projects, the permit timeline risk is lower than it was, though still real.

The provincial spending breakdown includes notable allocations for accelerated road and bridge repairs, dual-use infrastructure (facilities that serve both transit and utility functions), and energy-efficient school construction. These categories create specific procurement windows you can plan around.

Here is a numbered list of the four funding-driven priorities most relevant to Edmonton project managers in 2026:

- LRT expansion and transit-oriented development around new station areas

- School and healthcare construction funded through provincial capital budgets

- Municipal road construction and utility corridor upgrades across the city grid

- Affordable and multi-family housing supported by federal and provincial programs

Pro Tip: The most predictable project pipelines in 2026 are tied to already-approved public capital programs. If your business development strategy relies heavily on private development, consider whether adding one municipal or provincial stream could reduce your revenue volatility without adding much overhead.

Sector deep-dive: Navigating obstacles and sector shifts

Even with robust funding and policy support, not all sectors are riding the same wave. Let’s look closer at the practical realities on the ground.

The residential cooling is real but nuanced. Single-family starts have pulled back sharply in some suburban submarkets where speculative building ran ahead of actual buyer demand. Multi-family is more resilient, supported by rental demand and ongoing immigration. Project managers who built capacity around single-family volume should not assume the cycle will bounce back in the same form.

Industrial and logistics-related construction remains the strongest segment by occupier demand. Small-bay facilities, cold storage, and last-mile distribution centers are being fast-tracked wherever land and permits allow. This segment also tends to have more straightforward design requirements than institutional builds, which means shorter lead times and less exposure to design-change delays.

Contractors are getting more selective. That is not a complaint, it is a fact of the current Edmonton construction market. With capacity stretched and labor tight, experienced contractors are evaluating risk-to-return ratios more carefully. Projects with incomplete drawings, unclear scope, or aggressive schedules are getting fewer bids or being priced with large contingency allowances.

“In a seller’s market for construction capacity, the owner who submits the most prepared, well-scoped project package gets the best pricing and the best contractors.”

Cost pressures are hitting several categories simultaneously. Equipment costs are up due to fuel surcharges and fleet replacement cycles. Emissions regulations, while not yet the dominant compliance burden in Alberta, are already influencing equipment specifications for larger municipal contracts. Materials like concrete and asphalt have seen price volatility tied to energy costs and supply chain lead times.

Looking at concrete asset strategies and urban landscaping drivers together reveals something interesting: asset owners who invest in maintenance now are locking in lower unit costs before the next price escalation cycle hits in full.

A few common project management missteps specific to Edmonton’s 2026 environment:

- Starting procurement too late. With contractors selective, waiting until drawings are 100% complete before engaging the market costs time and leverage.

- Under-budgeting for winter construction. Edmonton’s climate adds real cost to year-round schedules, and this is still being underestimated on fixed-fee contracts.

- Ignoring market outlook signals. Managers who missed the industrial vacancy signals 18 months ago are now competing for space and capacity against better-positioned peers.

Pro Tip: Consider issuing a Request for Qualifications before finalizing your project documents. This tells you which contractors are actually available and interested, and it often surfaces constructability feedback that improves your drawings before bid.

Technology, labor, and procurement innovation

Sector challenges demand forward-thinking solutions. Next, let’s examine how Edmonton leaders are using technology and procurement to stay ahead.

The labor math is stark. Alberta faces 43,000 retirements by 2034, and the pipeline of new trades workers is not keeping pace. Non-residential employment in Alberta has grown about 8%, which sounds healthy until you realize it is being spread across a much larger volume of work. The result is that skilled labor is both more expensive and harder to retain on long projects.

This pressure is directly accelerating technology adoption. 81% of firms report productivity gains from implementing new technologies, and the tools getting the most traction in Edmonton’s market right now are:

- Building Information Modeling (BIM): Used not just for design coordination but for clash detection, quantity takeoffs, and sequencing. BIM reduces rework, which is one of the most expensive labor drains on any project.

- Modular and offsite fabrication: Mechanical rooms, washroom pods, and structural components pre-built in controlled environments save field labor hours and compress schedules.

- Robotic layout and automated grading: Total stations with robotic control and GPS-guided grading equipment are reducing the need for experienced field surveyors on repetitive tasks.

- AI-assisted scheduling and risk modeling: Software platforms are now good enough to flag scheduling conflicts and cost overruns before they materialize, giving managers earlier intervention windows.

On the procurement side, design-build and Integrated Project Delivery (IPD) models are gaining ground over traditional low-bid general contracting. The logic is straightforward: when labor and materials are tight, aligning contractor incentives with project outcomes reduces adversarial dynamics and improves delivery reliability. Owners who have switched to these models report better schedule performance even when overall costs are similar.

Choosing the right contractor in this environment means evaluating technology capability alongside price. A contractor who bids 5% lower but uses no BIM integration may end up costing more in coordination errors and schedule recovery.

Reviewing labor and capital forecasts for Alberta confirms that the pressure is not temporary. Structural workforce changes require structural procurement responses.

Pro Tip: If you are evaluating contractor proposals, add a section asking for their technology stack and how they use it on projects similar to yours. The quality of that answer will tell you a lot about how they manage risk.

What most Edmonton guides miss: The opportunity in selective growth

Most articles covering Edmonton’s construction boom focus on the size of the opportunity. Bigger pipeline, more projects, more revenue. The conventional wisdom is that a rising tide lifts all boats, so get as much work as possible.

The data does not support that logic right now. Contractors who overextended during the 2024 to 2025 residential surge are now managing strained cash flow, retention disputes, and quality callbacks. The ones doing well are the ones who said no to certain projects deliberately.

The real play for decision-makers in 2026 is selective growth. That means identifying which segments align with your actual capabilities, pursuing those with precision, and building deeper relationships with a smaller number of reliable partners rather than spreading thin across many marginal opportunities.

Industrial and public infrastructure projects are, in our view, the most underappreciated segments right now. They carry more predictable payment cycles, clearer scope, and funding that does not evaporate when interest rates move. Yet many managers and contractors still default toward residential because it feels familiar.

Strategic alliances matter too. The managers consistently landing better contractors, better pricing, and better schedules in this market are the ones who have invested in those relationships before the project scope is finalized. Reliability is a competitive advantage when capacity is constrained, and reliable partners do not appear on short notice.

The uncomfortable truth is that more projects is not better. Better projects, executed with the right partners at the right time, is what builds a durable position in Edmonton’s construction market over the next three to five years.

Take your next step with the right construction partner

Edmonton’s 2026 construction landscape rewards experience, local knowledge, and precise execution. With $43.3B in active projects, tightening contractor capacity, and sector shifts happening in real time, the difference between a well-managed project and a costly one often comes down to who you work with and how early you engage them.

At ProZone Ltd, we work directly with project managers and decision-makers on roads, concrete, asphalt, earthworks, and municipal infrastructure across Edmonton and the surrounding region. We understand the funding cycles, the permit environment, and the practical constraints that shape how projects move from planning to completion here.

If you are building out your project plan for 2026, start by exploring construction services tailored to Edmonton’s current market conditions. For road and pavement work specifically, our road construction solutions are built around the same predictable timelines and quality standards that public and commercial clients require. Reach out for a consultation or project quote and let’s talk about what your next project actually needs.

Frequently asked questions

What sectors are leading Edmonton’s construction growth in 2026?

ICI and infrastructure projects dominate Edmonton’s active pipeline by both project count and dollar value, while residential construction is moderating after the record 2025 surge. Industrial and institutional segments are the strongest performers heading into the remainder of 2026.

How is the labor shortage impacting Edmonton construction projects?

Workforce gaps are pushing firms toward BIM, modular construction, and robotic layout to maintain output. With 43,000 Alberta retirements expected by 2034, technology adoption is now a competitive necessity rather than a nice-to-have.

What are the most significant risks for managers in 2026?

Contractor selectivity, rising input costs, and a softening residential segment are the top risks. Contractors are pricing risk higher on poorly scoped projects, so managers who invest in thorough pre-construction documentation will see meaningfully better bid responses.

How much public funding is driving 2026 project activity?

Alberta’s capital plan commits $28.3B over three years, with $8.7B allocated in 2026 to 2027 alone, plus the City of Edmonton’s $1.5B annual infrastructure budget layered on top.

Which technologies are Edmonton builders adopting most?

BIM, modular fabrication, and AI-assisted scheduling lead adoption across the region. 81% of firms using these tools report measurable productivity gains, making technology capability a key factor when evaluating contractor proposals.